Lessor modifications

Finance leases

Lessor accounting for modification of finance leases is detailed in IFRS 16.79 to 80. Similar to lessee accounting, when the scope of a lease increases and the consideration changes commensurately, a separate lease exists. Where this is not the case, the lessor must:

- reassess the accounting for the lease and determine if the lease would have been considered an operating lease if the modification had been known; and, if so:

- create a new lease from the effective date of the modification; and

- reclassify the lease receivable balance at the date of modification to property, plant and equipment

- where the lease remains a finance lease, the lease receivable is remeasured by the application of IFRS 9. In such a case, assuming that that the receivable is classified as amortised cost, the change in future cash flows is a remeasurement event resulting in a gain or loss within profit or loss.

Operating leases

IFRS 16 provides only limited guidance on the modification of operating leases from a lessor’s perspective. It requires that any modification be considered a new lease, and that any remaining prepayments and accruals are included in the accounting for this new lease. IFRS 16 does not state whether balances arising from the lessor’s straight-lining calculation are considered to be accruals or prepayments but our view, consistent with the approach when applying IAS 17, is that they are.

In such an instance, if the new lease continues to be classified as operating, the future cash flows are recognised on a straight line (or other systematic) basis, adjusted for any prepayments or accruals. The expense recognition pattern should ensure the balance is written down to zero at the end of the lease.

Impairment

Due to the change in fair value of future cash flows, impairment indicators may exist such that impairment of the individual assets that are leased should be considered.

Lessee modifications

Reasssessment vs modification

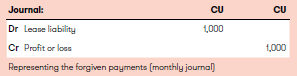

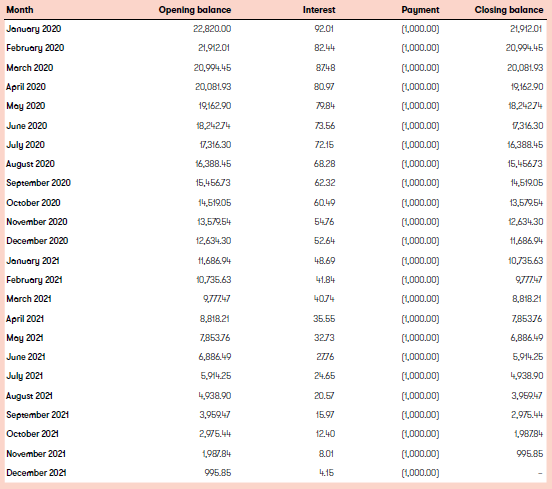

Lease modification and reassessment of the lease liability are two different concepts with potentially different accounting outcomes. Generally, a reassessment takes place when there are changes in lease payments based on contractual clauses included in the original contract – such as changes in CPI, a market price adjustment or a change in any price guarantee arrangement that might appear in the lease contract (IFRS 16.42). In such an instance, the lease liability is remeasured by discounting the future cash flows using the discount rate set in the initial measurement of the lease (IFRS 16.43).

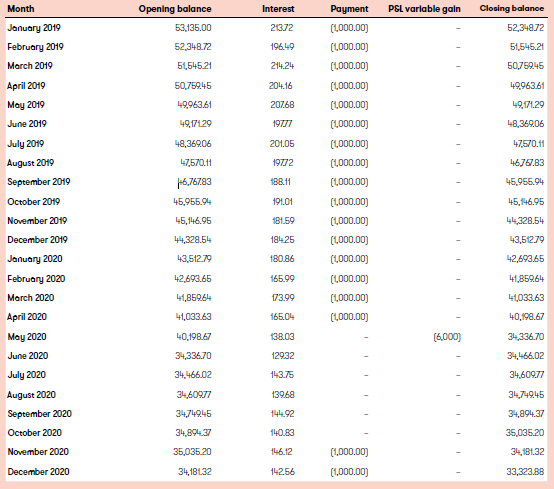

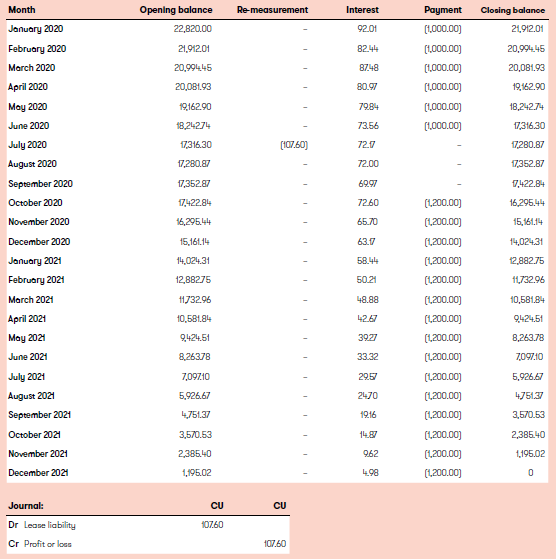

A lease modification (as considered in this document – does not address changes in the leased asset, such as decreases in leased space) arises when the lease contract is altered such that future cash flows and/or the scope of the lease changes. Where an increase in scope occurs, and the payment for this increase in scope is commensurate, a separate lease is accounted for (IFRS 16.44). Otherwise, the original lease is remeasured by:

Otherwise, the original lease is remeasured by:

- identifying a revised discount rate appropriate to the revised lease term, underlying asset and the lessee

- determining the net present value of future cash outflows using that revised discount rate

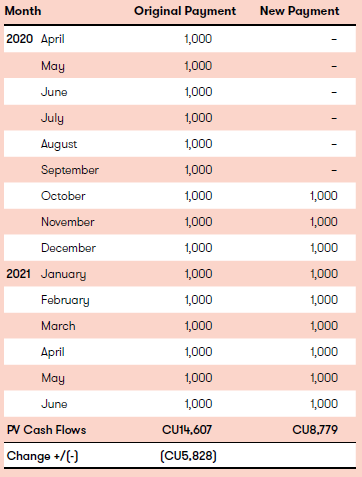

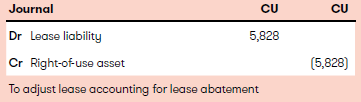

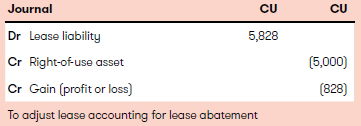

- adjusting the remaining right-of-use asset for the increase or decrease in the lease liability. If the adjustment exceeds the carrying value of the right-of-use asset this excess is recognised as a gain in profit or loss.