The European Financial Reporting Advisory Group (EFRAG) and then subsequently the European Commission, through its final consultation process, have provided some phased-In Disclosure Requirements that will help reporting entities, particularly smaller entities that would be subject to sustainability reporting requirements for the first time.

The full list of phased-in requirements is included in ESRS 1: Appendix C

A summary of phased-in Disclosure Requirements for all reporting entities is outlined below:

| Year 1 |

Year 2 |

Year 3 |

| Comparative information is not required |

|

| Datapoints related to their own workforce in ESRS S1 – social protection, persons with disabilities, work-related ill-health, and work-life balance are not required |

| Financial effects related to non-climate environmental issues (pollution, water, biodiversity, and resource use) are not required, qualitative disclosures can be provided in the first three years. |

| In the absence of sector-specific standards, other available frameworks could be used to develop specific disclosures if required for material entity-specific sustainability matters not included in the first set of ESRS. |

| Company-specific disclosures that were developed prior to the ESRS being adopted can still be used. |

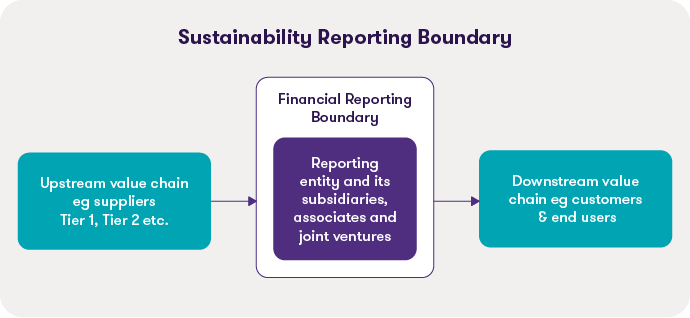

| There is a requirement to consider value chain as part of materiality assessment process but data gathering aspects are limited for the first three years and information on the value chain can estimated or omitted if the information is not available during this time. |

For reporting entities with less than 750 employees:

| Year 1 |

Year 2 |

Year 3 |

| Scope 3 Greenhouse Gas (GHG) emissions data, and ESRS S1 disclosures are not required. |

|

| The disclosure requirements for biodiversity (ESRS E4), Workers in the value chain (ESRS S2), Affected Communities (ESRS S3) and Consumers and End-users (ESRS E4) are not required. |

|

In addition, until 2030, EU subsidiaries of non-EU parents can prepare just one report, which includes subsidiaries that would ordinarily be required to report separately, due to size or if they are listed.